By Michael Lynch

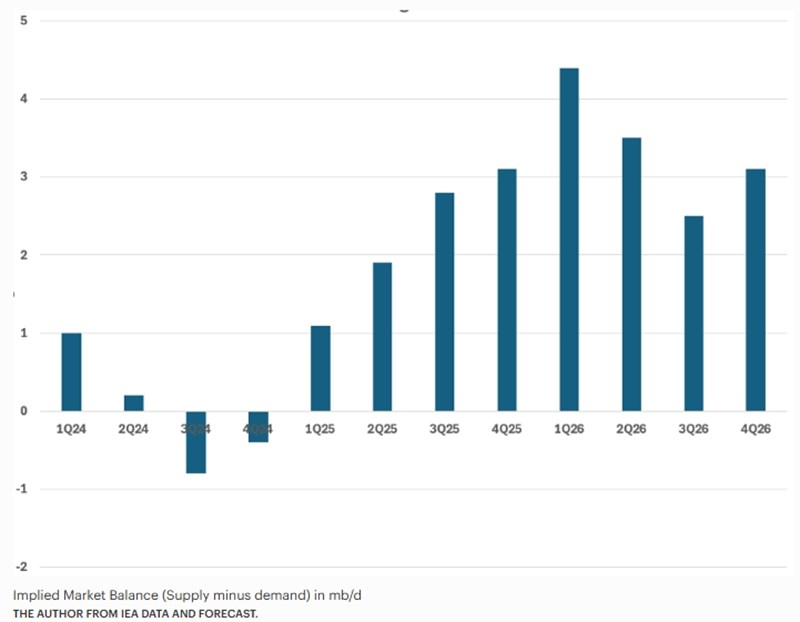

The internet is full of commentators who are worried about a possible oversupply of oil, as they say, despite the increase in reserves that seems to exist by 800 million barrels. barrels this year and by 1,200 million. barrels in 2026, according to the International Energy Agency (IEA), most of this increase does not show up in the data. The chart below shows the increase in inventories calculated based on global supply minus global demand and taking into account that OPEC production will remain stable from June 2025 to the end of 2026. The conclusion is that there will be a huge oversupply and an increase in inventories, conditions that are already putting pressure on prices.

Reactions include voices denouncing the international organization as incompetent or dishonest, while some argue that the failure to increase inventories suggests a much tighter market today and in the months to come compared to the IEA's forecast. To be sure, the International Energy Agency has repeatedly underestimated demand outside its member states, where data is usually insufficient. If this is the case today, the balance of the market is much less threatening than estimates.

Some criticisms are unfounded. The ILO's forecasts are biased, insofar as their authors are human – and people are biased. The same may be true for OPEC+ reports. There may also be institutional biases. The IOC has warned several times of imminent increases in oil prices, but now we have a forecast that speaks of an extremely weak market.

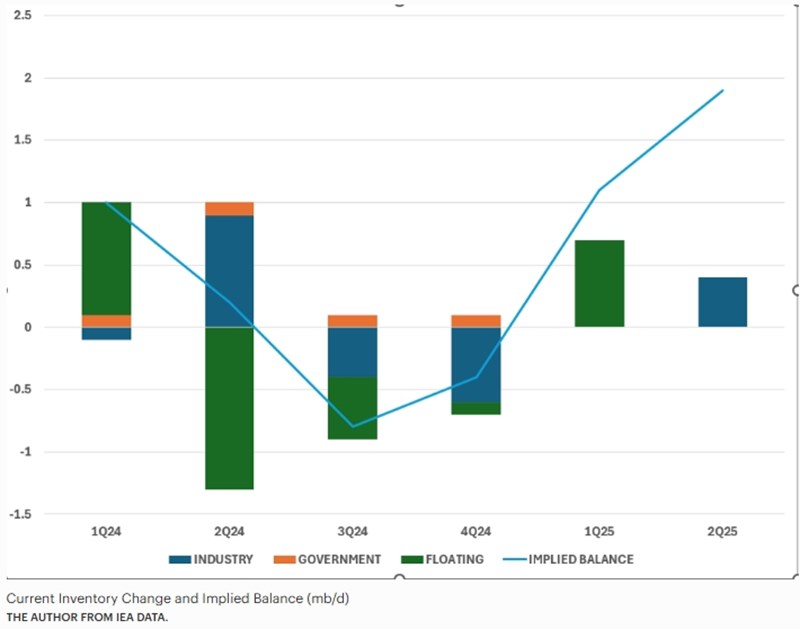

Undoubtedly, stocks are not behaving as they should. The chart below shows the changes in inventories compared to the balance (which is supply minus demand). The data for 2024 looks pretty good, with changes in inventories close to what would be expected. This changes this year, when there should have been a huge increase in inventories, about 500 million barrels, with 1.5 million barrels per day in the first half of the year, compared to the increase of 500,000 barrels per day observed.

Where is the missing oil? Stocks outside IEA member states are not included in the above figures and, given that half of oil consumption takes place outside the OECD, it would be expected that OECD stocks, as shown in the chart above, represent only half of the total. Even more important is the fact that, according to the IOC, from April to August 2025, China's reserves increased by 110 million tons. Barrels. (The IEA's estimate was 900,000 barrels per day from January to August). The increase in strategic oil reserves in China is supporting crude oil prices. This explains the difference without having to assume that demand is devalued by 1 million. barrels per day. It may be so, but then the stock picture would look much "tighter" than it looks today.

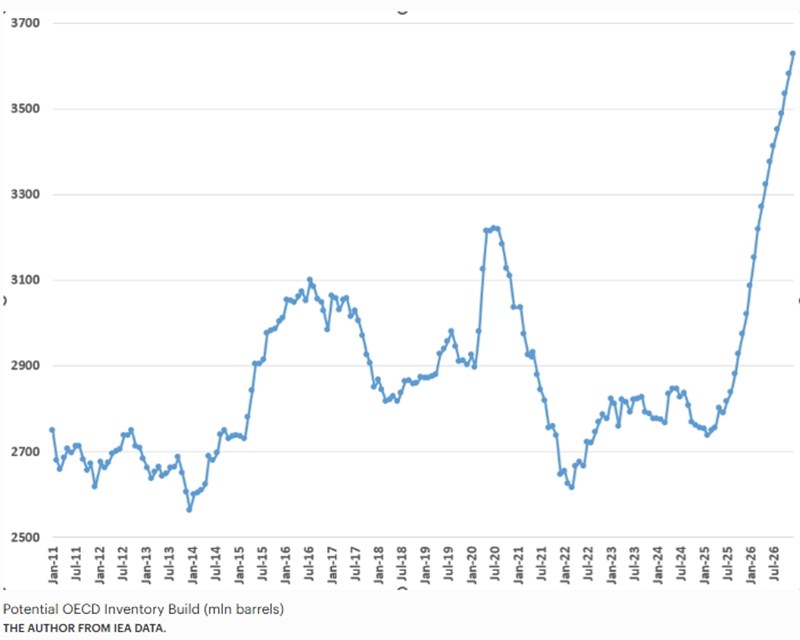

As regards the future course of the market, confidence in the balance of the market should be strengthened. Even if the estimates for demand are wrong by 1 million. barrels per day, the surplus in the market seems to exceed 2 million. barrels per day in 2026. If we assume that half of this oil ends up in the OECD reserves, as shown in the chart below, then it is difficult for the market to escape the grip of pressure in the coming months.

The nature of this year's increase in inventories, which appears to be largely concentrated in China's reserves, is significant, as the behaviour of state and commercial stockholders differs significantly. Commercial stockholders sometimes increase their stocks if they expect prices to rise and sell them if they think future prices will be lower, which exacerbates the price cycle. For their part, sovereign stockholders tend to buy and hold their stocks as a hedge against future supply disruptions, without taking into account market developments.

The Chinese government's purchase of stocks has three possible motives: a) the desired stock levels are determined by imports, which had increased, b) the possibility that Russian oil supplies will be affected by the sanctions leading them to increase their stockpiles in return, and c) the possibility that the government fears that some political controversy will lead to attempts to impose an embargo on oil markets. The latter could reflect either the Chinese government's plans to take certain aggressive measures that it fears will trigger an embargo, or simply the assessment that U.S. policies are so unpredictable that increased protection against a potential embargo is needed.

China's decision-making on the desired level of oil reserves is not clear. Changes are observed, but with a delay, while the motives that lead to buying or not buying are unknown. Since we don't know exactly why Beijing is increasing its strategic stockpiles or the target level it sets, future purchases (or sales) cannot be predicted. The -very likely- disruption of the markets means that the balance of the market could change quickly and drastically.

If the global economy is strong next year and sanctions against Iran, Russia and Venezuela become tighter, then the market balance could prove to be much tighter than the ILO's forecast. A surplus of €2 million. barrels per day is quite likely as an annual average, but in the first half we could see an increase in inventories, even if prices climb. This scenario would not be too difficult for markets to deal with, assuming that China continues to buy 1 million tons. barrels per day for its strategic reserves. However, a halt to these purchases by China would again threaten the market, and OPEC+ would have to intervene to prevent prices from collapsing.